After a record year in 2018, iDealwine’s strong momentum continues in 2019, with a promising first semester. Figures are rising, trends becoming clearer and phenomena emerging… This all leads us to believe that this year will once again be a successful year of auctions. We look back at the last six months.

2018 was a record year for iDealwine auctions. As of 31st December 2018, we recorded a total of €17.5 million (including fees) for 143,000 bottles sold. Similarly, 2019 got off to a pretty good start, and the first half of the year confirms the health of the market: the total sum exchanged on the iDealwine platform has already crossed the €10 million threshold, represented by more than 84,000 bottles having changed hands in six months. You might have done the math’s yourself: with volumes showing a rise of 15% compared to the first half of 2018, the price effect is clear: the increase in value amounts to 23%. The sign of a market seeking ever rarer, fine wines.

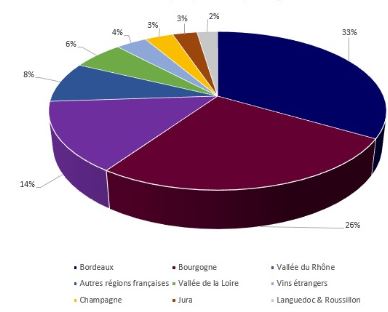

Share of sales by volume | S1 2019 auctions:

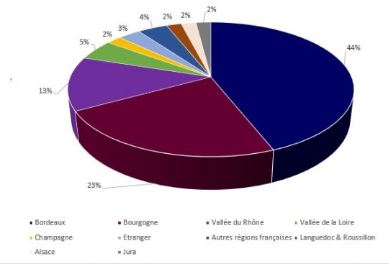

Share of sales by volume | 2018 auctions:

A total of 21 auctions were organized by way of our subsidiary IWA Auction, two of which were devoted to private collections (sourced from only one seller). Since the beginning of the year, some trends have been confirmed, while others are emerging. So what are the enophiles really looking for? As always, a share of the dream. Of course, the traditional regions of Bordeaux, Burgundy and the Rhone Valley make up the podium’s unrivalled trio, together representing 73% of trade.

Bordeaux remains in pole position in the first half of 2019, with a 33% share of volumes traded at auction, and 41% in value. Large formats (a jeroboam of Château Mouton-Rothschild 1986 sold for €7,296), rare wines in emblematic vintages (Château Clinet 1989 sold at €2,675) or historically significant (Crème-de-Tête 1945 from Château Gilette at €851) and old bottles (Château Pavie 1928) are the keys to its success. However, be warned: in this market, the increase in volume essentially concerns other regions, thus decreasing the share of Bordeaux at auction. For the record, at the end of 2018, Bordeaux Grands Crus still accounted for 44% of the volumes traded and 45% of the value sold. Concomitantly, Burgundy, which is in second place, continues its strong momentum, rising from 23% in volume at the end of 2018 to 26% at the close of the first semester. Unsurprisingly, the Domaine de la Romanée-Conti remains at the top of the most expensive bottles: a Romanée-Conti 2000 reached €14,957 last March.

The rise of the Rhone Valley is more discreet, but the region is, slowly but surely, on the up. With 8,000 bottles sold in the first semester, representing a 14% share of sales (compared with 13% at the end of 2018). Note that the most sought-after wines come primarily from the northern Rhône’s steep terraces, where mechanical work is impossible. Prestigious appellations (Hermitage, Côte-Rôtie, Cornas), cuvées that aren’t produced every year (Cathelin 1990 by Jean-Louis Chave sold at € 8,026) or domains that no longer exist (Côte-Brune 1985, the Côte-Rôtie of Marius Gentaz-Dervieux ) are at the centre of wine lover’s attention.

Yet despite the aura of prestige and mystery surrounding this vinous triptych, we have noted a proportional decrease on the whole (80% of wines traded in 2018 vs 73% in the first half of 2019) which opens the way for gems from unknown regions and foreign countries. Similarly, organic wines continue their breakthrough, today reaching 31% of sales. As a result, icons of the Loire such as Stéphane Bernaudeau (Les Nourissons 2012 sold at €207) and Richard Leroy (Les Noëls de Montbenault 2012) continue their ascent.

There’s no need to remind you that the charm of Champagne is down to the brilliance of its fine bubbles, its houses and iconic vintages. This northern region is also on the increase (3% of volumes traded compared to 2% in 2019), driven by enthusiasts’ interest in large formats (a Methuselah of Cristal 2002 Louis Roederer – €6,202), mature vintages (cuvée S 1959 from Salon – €4,134) and grower-producer champagnes (Dégorgement Tardif Jacquesson Signature 1989 – €372).

Proof of the sustained interest in organic, biodynamic and natural wines, the Jura has maintained its growth (3% of volume traded in the first half versus 2% in 2018 for this small wine region). If oxidative wines and old vintages are what enophiles set their sights on, names known for their natural winemaking have confirmed their star status (Pierre Overnoy with its 1990 Vin jaune sold for €1,763) while others are blazing (Vin de France Ja-Nai 2011 of Domaine des Miroirs, sold at €693).

It’s undeniable that in recent years, the Languedoc-Roussillon has risen from its ashes. As a result, enthusiasts have understood that as certain regions see their prices skyrocketing, the bottles are becoming scarce or require a long aging, it is worth exploring new, no less exceptional terroirs. New figures have therefore emerged and/or (re)discovered their potential in recent decades. Frédéric Pourtalié of Domaine Montcalmès is one of these leading lights (his Terraces du Larzac 2015 sold for €292), along with Hervé Bizeul of Clos des Fées (Côte du Roussillon La Petite Sibérie 2003 at €290).

That’s all for now but stay tuned: we’re currently preparing our regional auction analyses for this first semester before publishing them on the blog. As always, they will allow you to dig deeper into what’s happening in each of the French and foreign regions, to learn more about the stars – established or emerging – of the wine world.